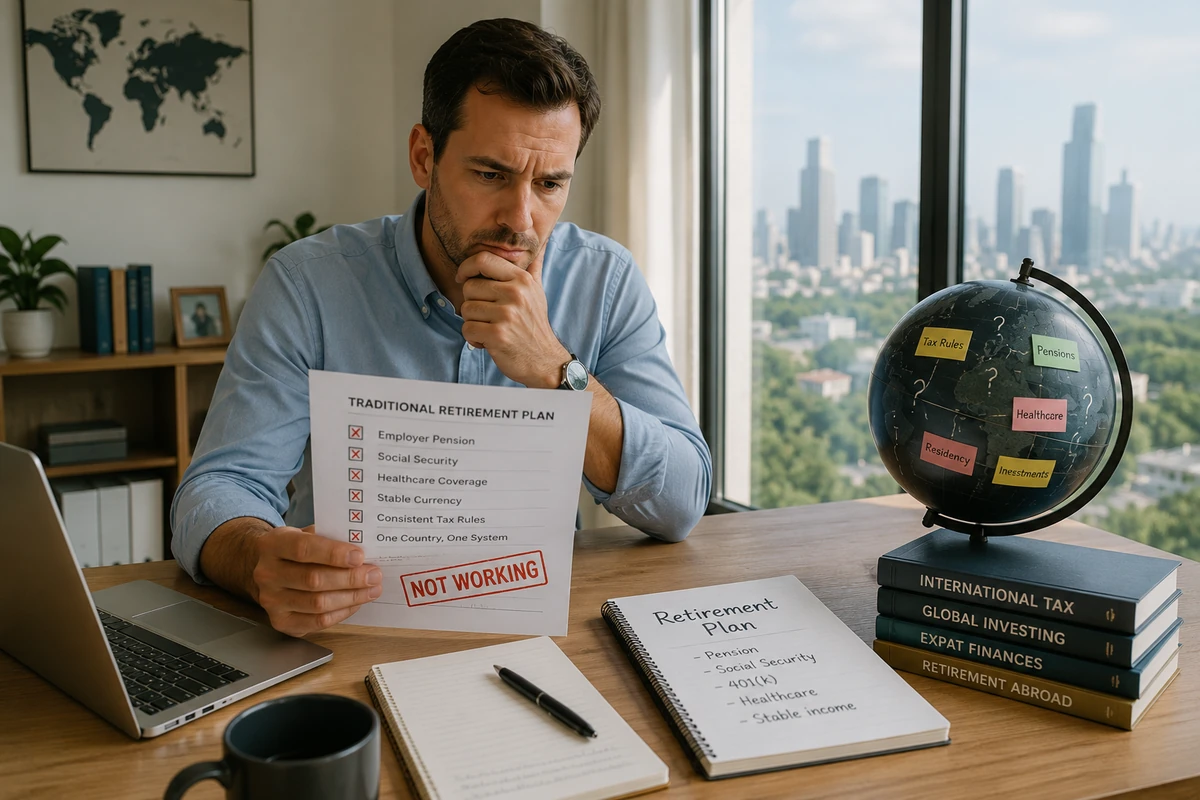

💼 Why Traditional Retirement Planning Fails Expats

TLDR

- Traditional retirement planning assumes a single country, single tax system, and stable long-term residency.

- Expats face cross-border tax rules, currency risk, and pension portability issues that standard advice rarely addresses.

- Citizenship-based taxation and residency-based taxation create very different long-term planning realities.

- Public pension eligibility often depends on contribution history and bilateral agreements between countries.

- Successful expat retirement planning requires flexibility, jurisdiction awareness, and globally diversified assets.

Most retirement advice is built around a quiet, unexamined assumption: you will live, work, and eventually retire in the exact same country. For globally mobile individuals and international families, that foundational assumption falls apart almost immediately.

If you are currently raising children in Latin America or Asia while holding legal citizenship somewhere else, earning income across multiple currencies, and potentially planning another major international move down the road, the standard financial blueprint simply does not fit your reality.

It is not that mainstream financial advice is inherently wrong; it is just dangerously incomplete.

For an active international parent, navigating these structural gaps is an essential part of understanding what is an expat father and a long-term provider. Let us break down exactly where traditional models break down and how you can map out a highly resilient, cross-border financial future.

🗺️ The Flawed Single-Country Assumption

Traditional financial building models are built entirely on a highly predictable, linear life path. You are expected to work in one domestic economy for 30 to 40 consecutive years, contribute diligently to a single national pension system, and accumulate your investments in tax-advantaged accounts operating under one cohesive tax code.

Finally, you retire locally and draw your distributions in the exact same currency you used to pay your bills for decades.

Expat life completely disrupts every single stage of that process. You might split your primary working years across three or four distinct countries over a twenty-year period. This creates unique challenges for anyone attempting comprehensive expat retirement planning on their own.

| Retirement Phase | Standard Linear Model | The Expat Reality |

| Working Income | Single domestic currency | Multi-currency income sources |

| Tax Framework | One tax code for life | Overlapping tax jurisdictions |

| Asset Location | Domestic bank or brokerage | Accounts scattered globally |

| Endpoint Geography | Retiring in the same country | Moving to a new target nation |

Standard online retirement calculators are not programmed to ask these nuanced questions. They fail to account for the unique friction points faced by globally mobile families.

Overlooking these structural differences is one of the most common ways parents end up unintentionally hindering how they map out how expat families build long-term stability across borders.

📑 Pension Portability Is Not Automatic

Public state pension systems are almost universally based on strict lifetime contribution histories. Your ultimate eligibility depends heavily on meeting specific minimum years of active contributions and hitting defined age requirements.

In many countries, if you choose to emigrate before reaching that minimum contribution threshold, you may lose your accumulated entitlements entirely.

Fortunately, some countries maintain formal international agreements to coordinate social security coverage. These bilateral frameworks help prevent double contributions and protect your benefit rights when moving.

Expert Tip: You can review the operational details of these cross-border coordination programs by examining the official overview of social security totalization agreements. Always check the exact treaty parameters between your home country and host nation.

If you happen to move between countries that lack these specific bilateral agreements, your accumulated contribution years will not combine. This can easily lead to highly fragmented entitlements.

Navigating these fragmented systems is a core aspect of handling expat pension planning properly, ensuring you do not leave valuable money on the table when moving between different systems.

🏛️ Citizenship-Based Taxation Complicates Everything

The vast majority of nations across the globe choose to tax individuals based strictly on their physical residency status. If you reside within their borders long enough to satisfy their local residency criteria, you are taxed on your worldwide income.

However, if you officially pack up, leave the territory, and break your local residency ties, you generally stop being taxed as a resident.

The United States stands as a notable exception to this global norm. It utilizes a system of citizenship-based taxation, meaning U.S. citizens are taxed on their global income regardless of where they sleep.

Tax Framework Comparison:├── Residency-Based: Taxation stops when you legally break local ties└── Citizenship-Based: Global reporting continues regardless of physical locationThis structural reality introduces significant administrative friction for families trying to organize their retirement savings abroad efficiently. While foreign tax credits can often mitigate double taxation, the compliance reporting obligations remain intense.

It forces expat dads to analyze both sides of the border carefully, matching their tax strategy with standard expat taxes made simple for families living abroad guidelines.

🏦 Retirement Accounts Do Not Always Translate

Tax-advantaged retirement accounts are country-specific by design. Frameworks like 401(k) plans, IRAs, superannuation funds, provident funds, and traditional national pension schemes are all built exclusively around domestic tax laws.

The underlying contributions, investment growth, and eventual withdrawals are all treated differently depending on the specific legal jurisdiction.

If you choose to relocate internationally, your new country of residence may completely refuse to recognize the tax-deferred status of your foreign accounts. While specific bilateral tax treaties provide protection in certain situations, many common expat paths are not covered.

- Tax Treatment: Foreign jurisdictions may tax the annual internal growth of your home-country accounts.

- Distribution Penalties: Withdrawing funds while living overseas can trigger unexpected local tax liabilities.

- Reporting Fines: Failing to declare foreign accounts can result in severe financial penalties.

Traditional retirement planning assumes your financial nest egg will remain comfortably nestled within a single, predictable tax framework for life.

Because international parents typically operate across two or more systems simultaneously, learning how to invest as an expat without breaking tax rules becomes a mandatory step in avoiding catastrophic financial surprises later.

💱 Currency Risk Is Often Completely Ignored

Mainstream retirement projections assume completely stable, predictable purchasing power within a single domestic currency.

However, if you spend decades accumulating your core assets in U.S. dollars or Euros but ultimately plan on retiring in a country like Thailand, Mexico, or Malaysia, unexpected exchange rate fluctuations will directly dictate your actual daily lifestyle.

Currency movements are driven by complex shifts in international inflation, interest rate differentials, and broader macroeconomic indicators. Over extended time horizons, these currency fluctuations can become massive.

Expert Tip: To insulate your family against currency volatility, aim to align at least a portion of your long-term investment portfolio directly with the specific currency you intend to spend during retirement.

Failing to plan for currency exposure is one of the most dangerous expat retirement pitfalls. Standard domestic advice rarely mentions this because it assumes your income and expenses will always match perfectly.

For global households, managing currency alignment is just as critical as selecting standard banking options for long-term expat families.

🩺 Healthcare Systems Vary Dramatically Across Borders

Access to reliable healthcare is a primary structural pillar of any functional retirement plan. In several countries, retirees rely almost exclusively on public medical systems funded through their prior working contributions.

In other regions, private international medical insurance or direct out-of-pocket payments are the norm.

If you choose to switch countries at the point of retirement, your access to local public healthcare will not automatically follow you across the border. Many nations enforce mandatory residency wait periods before you can enter their public health infrastructure.

| Healthcare Metric | Public System Access | Private Insurance Model |

| Funding Source | Prior local tax contributions | Monthly or annual premium payments |

| Portability | Restricted to specific nations | Globally portable across borders |

| Eligibility | Dependent on legal residency status | Dependent on age and medical history |

This is one specific area where complete clarity matters far more than blind optimism. If you are building a life overseas, understanding your medical coverage options is vital.

It is why smart parents look into health insurance mistakes expats make and how to avoid them long before they ever reach their target retirement age.

📉 The 4 Percent Rule Was Never Designed for Global Mobility

The highly popular, standardized withdrawal strategies frequently cited in retirement seminars are based heavily on historical market data.

These classic formulas assume a portfolio denominated in one currency, living expenses anchored in that identical currency, and a retirement spent entirely within that specific economic environment.

When you layer in cross-border taxation, foreign exchange exposure, and the logistical realities of retiring overseas challenges, the baseline mathematical models shift completely.

- Sequence Risk: Currency drops combined with market downturns can accelerate portfolio depletion.

- Tax Drag: Unrecognized foreign tax structures can cut your net safe withdrawal rate significantly.

- Transfer Fees: Moving money across borders regularly introduces ongoing banking friction.

This reality does not invalidate the importance of maintaining a disciplined withdrawal strategy. It simply means your financial strategy must be adapted to your unique geographical footprint.

Your plan should always reflect where you actually plan to spend your time, not where an outdated academic model assumes you will live.

🎈 Inflation Is Not a Universal Metric

Mainstream financial models almost always bake in a generic, domestic inflation rate when projecting your future purchasing power. In reality, inflation rates vary wildly from one country to another based on local monetary policy and supply chains.

Read More: To better understand the structural reasons why macroeconomic trends fluctuate across different regions, read through the historical analysis of why inflation differs across countries.

If you choose to settle in a country suffering from high local inflation while your core assets remain tied to a foreign currency, your real-world purchasing power can erode much faster than your financial planner anticipated.

Conversely, some households use this to their advantage by practicing geographic arbitrage, moving to locations with a lower cost of living to instantly extend the life of their portfolio.

⚖️ Estate and Succession Laws Add Another Complex Layer

Comprehensive financial planning is not just about generating monthly income; it is also about ensuring the smooth, safe transfer of family assets to the next generation. International inheritance and succession rules vary drastically between legal jurisdictions.

Some countries enforce rigid forced heirship rules that legally dictate exactly how your estate must be divided among your children. Other nations offer complete testamentary freedom, allowing you to distribute your assets precisely as you see fit.

- Jurisdictional Conflicts: Real estate is almost always governed by the laws of the country where the land is physically located.

- Probate Delays: Holding accounts across multiple countries can freeze assets for months during legal transitions.

- Guardianship Laws: Local courts may decide child custody differently than your home country will.

Traditional advice completely ignores cross-border succession planning. For international fathers, ensuring your assets are structured correctly across jurisdictions is an essential part of learning how to save for your child’s future while living abroad without leaving behind a massive legal mess.

🚀 A Better Framework for International Wealth

So if traditional models fall short, what actually works for an international family? The answer lies in building a flexible, location-independent financial foundation.

This requires stepping away from rigid domestic schemes and designing a global retirement strategy centered around true geographic optionality.

Focus on building globally diversified investment portfolios that are not tethered to the health of a single domestic economy. Ensure you maintain a deep, clear understanding of how your assets are taxed by both your country of legal citizenship and your current country of residence.

Expat Wealth Pillars:├── Maintaining highly portable, globally diversified brokerage accounts├── Aligning asset currencies with intended future lifestyle destinations└── Keeping emergency funds liquid across secure international banking hubsMap out your expected long-term living arrangements with clear milestones. If you are still entirely unsure where you will end up, build maximum optionality into your architecture by keeping your assets fully portable.

This mindset shifts your focus toward building sustainable global cash flow, allowing you to master multi-currency family budgeting for expat families with total confidence.

🛠️ Avoiding Retirement Planning Mistakes Overseas

The most powerful mental shift you can make is moving entirely away from a static mindset toward a dynamic financial independence framework.

This means prioritizing cross-border asset resilience and flexible cash generation over a fixed, unyielding geographic endpoint. It changes how you evaluate risk on a daily basis.

- Audit Regularly: Review your contribution records across all historical state pension systems.

- Maintain Buffers: Keep a liquid multi-currency cash cushion to handle unexpected exchange rate drops.

- Seek Specialization: Partner with international tax specialists who understand cross-border compliance.

Taking these steps ensures you are actively avoiding retirement planning mistakes overseas. It transforms financial planning from a source of ongoing anxiety into a structured, manageable workflow that protects your household.

🏁 Conclusion: Retirement Is a Jurisdiction Strategy

Traditional retirement planning fails expats because it is built entirely on the fragile assumption of geographic permanence. Expat life, by its very nature, is built on mobility.

Different tax frameworks, volatile currencies, uncoordinated pension schemes, and conflicting healthcare systems intersect in complex ways that mainstream financial advice simply cannot address.

But that is completely fine. It simply means you need to utilize a much broader lens. When you treat retirement planning as an active jurisdiction strategy rather than a single-country event, your financial path becomes clear.

You design for total asset portability, account proactively for shifting tax residencies, and align your investment currencies with your family’s future lifestyle goals.

For fathers focused on building an independent, highly stable future for their households overseas, intentional design beats traditional advice every single time.